Step-By-Step: Exactly How to Acquisition a Reverse Home Loan With Self-confidence

Browsing the complexities of acquiring a reverse home mortgage can be challenging, yet a systematic approach can encourage you to make educated decisions. It starts with examining your eligibility and understanding the nuances of different loan options available in the market (purchase reverse mortgage). As we explore each action, it becomes noticeable that confidence in this financial decision copyrights on detailed prep work and educated options.

Comprehending Reverse Home Mortgages

The primary device of a reverse mortgage involves loaning against the home's worth, with the financing quantity enhancing over time as passion builds up. Unlike standard home loans, customers are not needed to make monthly repayments; instead, the lending is paid back when the home owner markets the property, leaves, or dies.

There are 2 primary kinds of reverse home mortgages: Home Equity Conversion Home Mortgages (HECM), which are federally guaranteed, and proprietary reverse mortgages provided by private lending institutions. HECMs usually give higher defense due to their regulative oversight.

While reverse home mortgages can provide monetary alleviation, they also come with prices, consisting of source charges and insurance policy costs. Consequently, it is vital for prospective consumers to fully recognize the terms and effects before waging this financial choice.

Evaluating Your Eligibility

Eligibility for a reverse home loan is mostly figured out by several key variables that possible borrowers need to consider. Firstly, candidates should be at least 62 years of age, as this age requirement is established to ensure that consumers are coming close to or in retired life. In addition, the home has to act as the consumer's key residence, which means it can not be a holiday or rental building.

Another important element is the equity placement in the home. Lenders generally call for that the consumer has an enough amount of equity, which can affect the quantity readily available for the reverse mortgage. Generally, the extra equity you have, the bigger the finance quantity you may receive.

Moreover, potential consumers should show their capacity to fulfill economic commitments, including residential property taxes, homeowners insurance, and upkeep costs - purchase reverse mortgage. This evaluation frequently consists of a financial analysis performed by the lender, which reviews income, credit report, and existing debts

Last but not least, the home itself need to meet details criteria, including being single-family homes, FHA-approved condos, or specific manufactured homes. Recognizing these elements is necessary for identifying qualification and planning for the reverse home mortgage procedure.

:max_bytes(150000):strip_icc()/dotdash-reverse-vs-forward-mortgage-Final2-6961b02571a444ec8bfad146b6138665.jpg)

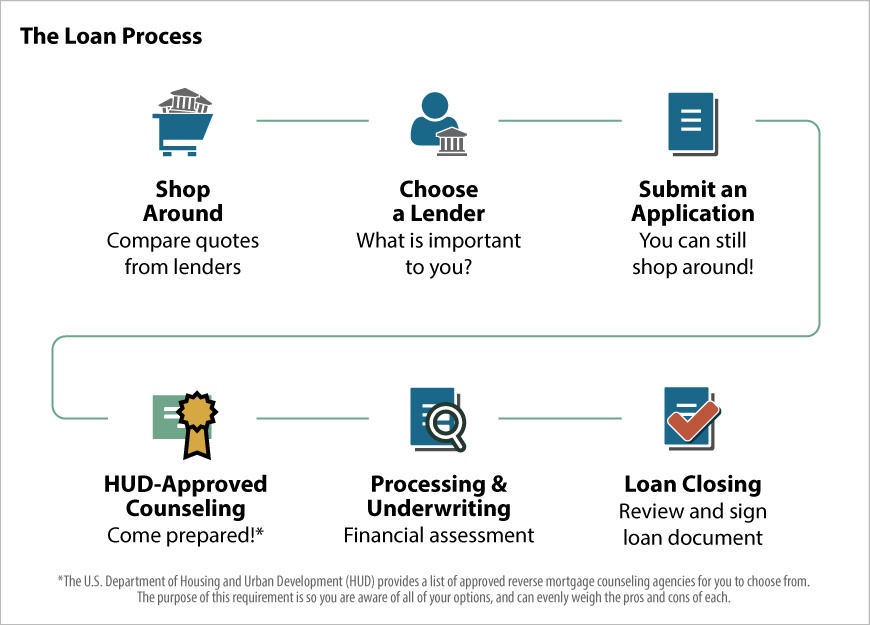

Researching Lenders

After determining your qualification for a reverse home mortgage, the following action includes investigating lenders who provide these economic products. It is critical to determine reliable loan providers with experience in reverse home loans, as this will ensure you receive reliable assistance throughout the process.

Begin by examining lending institution credentials and qualifications. Search for lenders that are participants of the National Opposite Mortgage Lenders Association (NRMLA) and are approved by the Federal Housing Management (FHA) These associations can suggest a dedication to honest techniques and compliance with industry criteria.

Reading customer testimonials and endorsements can give understanding into the lending institution's track record and client service click now high quality. Websites like the Better Business Bureau (BBB) can also provide rankings and issue histories that may assist inform your decision.

Additionally, talk to financial consultants or housing therapists who concentrate on reverse home loans. Their experience can help you navigate the alternatives readily available and suggest reliable loan providers based upon your distinct economic circumstance.

Comparing Lending Options

Comparing lending alternatives is an important step in safeguarding a reverse mortgage that straightens with your financial objectives. When assessing numerous reverse home loan items, it is important to consider the certain features, costs, and terms associated with each alternative. Start by examining the kind of reverse mortgage that finest matches your needs, such as Home Equity Conversion Home Loans (HECM) or proprietary loans, which may have various qualification requirements and benefits.

Following, take notice of the rate of interest and fees related to each financing. Fixed-rate fundings give stability, while adjustable-rate alternatives might offer lower preliminary prices yet can fluctuate in time. Furthermore, take into consideration the ahead of time expenses, including home mortgage insurance premiums, origination charges, and closing expenses, as these can dramatically impact the overall cost of the finance.

Furthermore, analyze the repayment terms and how they align with your long-term financial strategy. When the loan must be paid off is crucial, comprehending the ramifications of exactly how and. By thoroughly comparing these variables, you can make an educated choice, ensuring your selection sustains your monetary wellness and provides the security you look for in your retirement years.

Completing the Purchase

As soon as you have very carefully examined your options and selected one of the most appropriate reverse mortgage item, the next action is to settle the acquisition. This procedure includes several essential actions, guaranteeing that all essential paperwork is accurately finished and sent.

First, you will require to gather all required documents, including evidence of income, real estate tax statements, and homeowners insurance policy documentation. Your lending institution will give a listing of details files required to promote the approval procedure. It's essential to give precise and full details to prevent hold-ups.

Next, you will certainly undergo a detailed underwriting process. Throughout this stage, the lender will analyze your financial situation and the worth of your home. This might include a home evaluation her response to establish the home's market worth.

As soon as underwriting is full, you will receive a Closing Disclosure, which details the last terms of the financing, including charges and rate of interest. Evaluation this record carefully to guarantee that it lines up with your assumptions.

Verdict

Finally, navigating the process of purchasing a reverse home mortgage requires an extensive understanding of qualification requirements, thorough study on lending institutions, and mindful contrast of loan choices. By systematically complying with these steps, individuals can make informed decisions, ensuring that the selected mortgage aligns with economic goals and demands. Ultimately, a knowledgeable approach cultivates confidence in protecting a reverse mortgage, providing monetary you can find out more security and support for the future.

Look for lenders who are participants of the National Opposite Home Loan Lenders Association (NRMLA) and are approved by the Federal Real Estate Management (FHA)Contrasting finance choices is an important step in securing a reverse home mortgage that lines up with your economic goals (purchase reverse mortgage). Beginning by reviewing the type of reverse mortgage that ideal fits your needs, such as Home Equity Conversion Home Mortgages (HECM) or exclusive fundings, which might have various eligibility standards and benefits

In conclusion, navigating the procedure of buying a reverse mortgage calls for a complete understanding of qualification requirements, attentive research study on lenders, and mindful comparison of financing choices. Inevitably, a knowledgeable strategy cultivates self-confidence in protecting a reverse mortgage, supplying monetary security and support for the future.

Comments on “Why You Should Purchase Reverse Mortgage to Secure Your Future”